Tens of millions of small business owners built something real over decades. Now they are retiring, and most of them have no succession plan. For investors who understand the SMB investment landscape, that reality is not a problem to solve. It is one of the most durable opportunity pipelines in private markets today.

At SMB Value Investing Group, we think about the SMB market in two distinct layers: the sheer volume of businesses approaching a transition event, and the economic weight sitting behind them. Understanding both is what separates investors who see this as a niche play from those who recognize it as a generational window.

The Scale of What Is Coming

The numbers, when you actually sit with them, are staggering. A widely cited U.S. Small Business Administration estimate suggests that approximately 10 million Baby Boomer-owned businesses will change hands between 2019 and 2029. That is not a projection built on optimism. It is a demographic inevitability tied to the retirement timelines of the largest generation of business owners in American history.

Project Equity’s research adds another layer of urgency. Their analysis identifies 2.3 million employer businesses owned by aging Boomers that are at genuine risk of closure if no succession solution emerges. These are not distressed companies. Many are profitable, community-rooted businesses that simply lack a next owner. That closure risk is what creates the supply-side conditions for a compelling SMB investment opportunity that cannot be easily replicated in any other segment of the market.

| Metric | Number | Source |

| Boomer businesses changing hands | ~10 Million (2019-2029) | U.S. SBA Estimate |

| Employer businesses at closure risk | 2.3 Million | Project Equity |

| Firms in Silver Tsunami cohort | 2.9 Million | Project Equity |

| Workers employed by those firms | ~32 Million | Project Equity |

| Annual revenue at risk | ~$6.5 Trillion | Project Equity |

| Owners without an exit plan | Less than 1 in 3 | Teamshares Research |

Project Equity’s broader Silver Tsunami analysis sizes this cohort at roughly 2.9 million firms employing 32 million workers and generating approximately $6.5 trillion in annual revenue. That figure does not imply all of this becomes immediately acquirable. But it does tell you that the ownership transition pipeline is deep enough, and long enough, to sustain serious acquisition activity well into the next decade.

“This is not a one-year trade. It is a 10-plus year demographic pipeline with a long tail — and most of the capital that should be addressing it has not shown up yet.”

The Economic Weight Behind the Numbers

It is worth pausing on what $6.5 trillion in revenue actually represents in context. That figure, tied to businesses owned by aging founders with no clear succession path, is larger than the GDP of every country in the world except the United States and China. The point is not to be dramatic. The point is that the opportunity is structural, not cyclical, and the assets sitting inside it are real operating businesses with customers, cash flow, and decades of operating history.

For investors engaged in value investing for SMBs, that combination matters enormously. You are not acquiring speculative growth stories or pre-revenue concepts. You are acquiring businesses that have already proven themselves in the market and need a thoughtful transition rather than a transformation. That distinction changes the risk profile in ways that most traditional asset classes simply cannot offer.

Why the Market Stays Inefficient Despite Growing Interest

One of the most common objections to the SMB thesis is that increasing capital flows will eventually compress the opportunity. More search funds, more independent sponsors, more institutional interest – surely that erodes the edge? The data, and the structural reality on the ground, suggests otherwise.

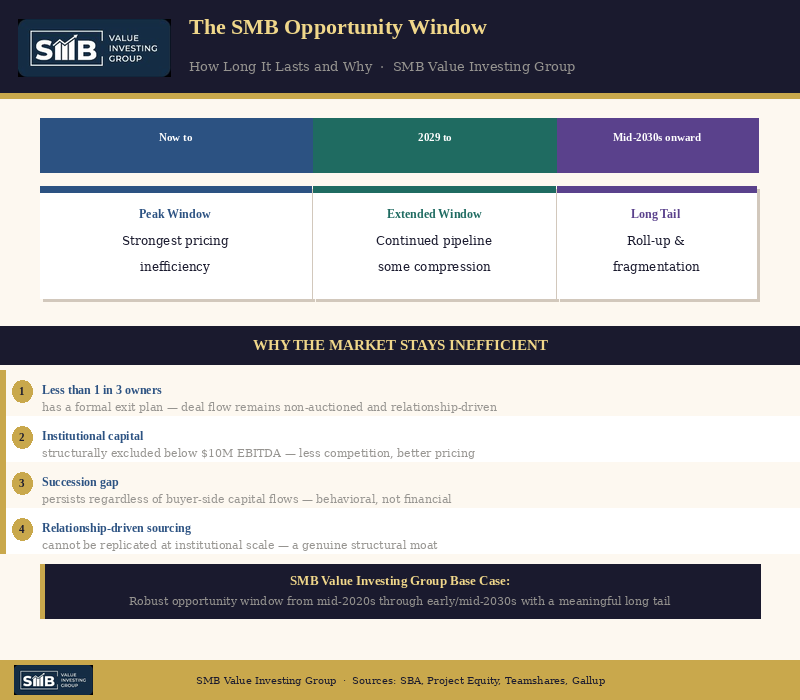

The core reason is behavioral, not financial. Teamshares research finds that fewer than one in three small business owners has a formal exit plan in place. Gallup’s work on succession planning reinforces this: the gap between retirement intention and actual planning is enormous, particularly among non-employer businesses. What this means practically is that a large portion of motivated sellers are arriving at the transaction table without preparation, without a banker, and without a competitive process. That is the definition of an inefficient market.

The small business investment process that works in this environment is one built around trust, patience, and the ability to work directly with owners who have never sold a business before. That kind of relationship-driven sourcing is not something that scales easily with institutional capital. It is a genuine structural moat.

| Market Condition | What It Means for Buyers | Why It Persists |

| Less than 1 in 3 owners has an exit plan | Non-auctioned, relationship-driven deal flow | Owner behavior does not change with buyer-side capital |

| 2.3M businesses at closure risk | Motivated sellers without competitive processes | Demographic pressure continues through the 2030s |

| Most businesses in $2-10M EBITDA band | Below minimum check size for large PE funds | Institutional capital structurally excluded |

| Limited banker coverage at lower end | Direct seller access, lower intermediary costs | Economics do not support full advisory mandates |

How Long Does the Window Stay Open?

The honest answer is longer than most people assume. If you anchor on the SBA’s core transition estimate as running from 2019 through 2029, you are looking at a sustained pipeline through the end of the decade at minimum. But the reality is more nuanced than that. Business owners do not retire on a fixed schedule. Many delays. Many attempt internal succession first and discover it does not work. Many recapitalize before eventually selling. The 2029 date is a midpoint, not a cliff.

Project Equity’s analysis makes the case that the pressure continues beyond any single year because the underlying risk — profitable businesses closing without a buyer — does not resolve itself without an active acquisition ecosystem. The base case at SMB Value Investing Group is a robust opportunity window running from the mid-2020s through the early-to-mid 2030s, with a meaningful long tail beyond that driven by fragmentation and roll-up dynamics.

| Time Horizon | Primary Driver | Expected Conditions | Opportunity Quality |

| Now through 2029 | Peak Boomer retirement wave | High volume, motivated sellers, limited planning | Strongest pricing inefficiency |

| 2029 through mid-2030s | Delayed transitions and closure pressure | Continued pipeline, some multiple compression | Strong with disciplined sourcing |

| Mid-2030s onward | Fragmentation and roll-up dynamics | Active M&A, platform strategies dominant | Returns driven by operational excellence |

What This Means for the Investment Thesis

The SMB market is large because it is structural. Millions of owner-operated businesses are approaching a transition event, and the gap between the number of motivated sellers and the number of prepared, relationship-oriented buyers remains wide. The result is a persistent supply of quality companies in the $2 million to $10 million EBITDA range where pricing stays meaningfully below what larger PE markets would apply to equivalent cash flow profiles.

For those building a disciplined small business investment process, the conditions are as favorable as they have been at any point in the past two decades. The pipeline is deep, the sellers are motivated, and the market structure rewards patient capital over financial engineering. That is not a common combination in private markets today.

At SMB Value Investing Group, we have spent considerable time stress-testing this thesis against the concern that growing interest in search funds and independent sponsorship will compress returns over time. Our conclusion is that the market is large enough, fragmented enough, and behaviorally inefficient enough that disciplined buyers with genuine sourcing infrastructure will continue to find compelling value investing for SMBs opportunities well into the next decade.

The Bottom Line

The SMB investment opportunity is not a narrative. It is a demographic reality backed by measurable data across millions of businesses, tens of millions of workers, and trillions of dollars in economic output. The window is open now, the structural drivers are well understood, and the market remains, by almost every measure, underserved by qualified buyers.

For investors who are willing to engage with the complexity that this market requires, that gap represents one of the most durable and defensible alpha opportunities in private markets over the next ten to fifteen years. Not because the opportunity is hidden, but because it demands a kind of patient, relationship-driven capital that most institutions are not set up to deploy.