Exit Options and Sources of Liquidity in SMB Acquisitions

How investors in the lower middle market actually realize returns and why liquidity is less mysterious than most people assume.

There’s a narrative that tends to follow private SMB investing around like a shadow: the idea that once your capital is deployed into a small business, it’s stuck there indefinitely, waiting for some elusive buyer to show up. That story is mostly fiction and at SMB Value Investing Group, we’ve found it’s worth addressing directly.

The reality is that well-run small and mid-sized businesses operate within one of the most active private M&A ecosystems in the country. According to PitchBook (2024), the lower middle market, broadly defined as businesses with enterprise values between $5M and $50M, has seen record transaction volume since 2020. Thousands of deals close annually across services, manufacturing, distribution, and beyond. Liquidity isn’t theoretical in this space. It’s demonstrated repeatedly, quarter after quarter.

That said, the path to liquidity in SMB investing looks different from public markets. It requires patience, planning, and deliberate execution. At SMB Value Investing Group, we underwrite every acquisition with multiple realistic exit scenarios already mapped out, not as an afterthought, but as a core part of the SMB investment criteria we apply before committing a single dollar.

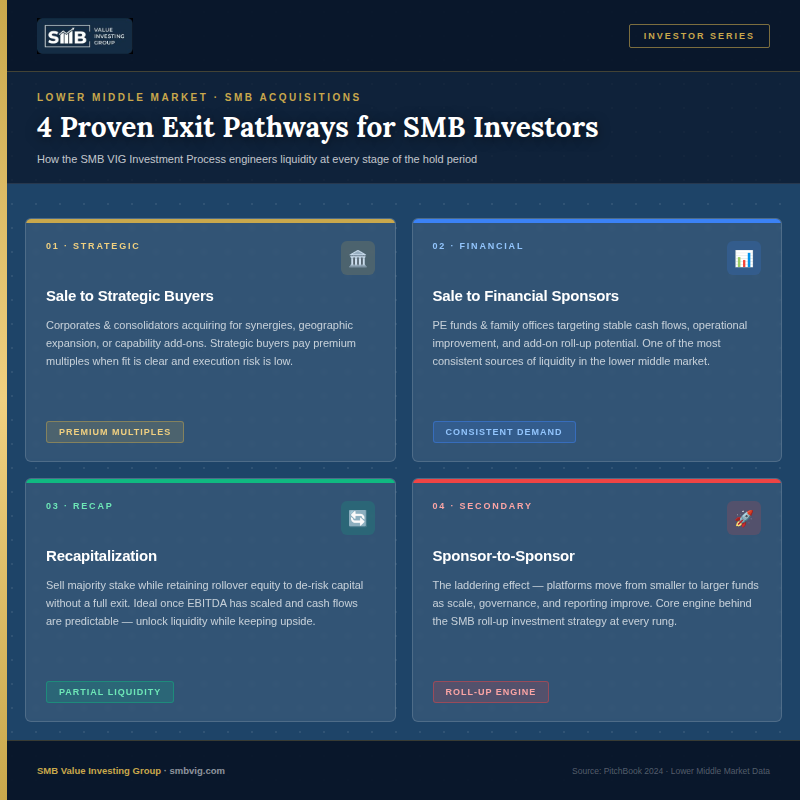

The Four Primary Exit Pathways

Across the lower middle market, exits generally fall into four categories. Understanding how each one works and when it makes the most sense is a big part of what separates disciplined investors from those who are simply hoping for the best.

Sale to a Strategic Buyer

Strategic acquirers are operating companies looking to grow through acquisition rather than organic expansion alone. They might be larger players in the same industry seeking geographic reach or corporate buyers after a specific capability, customer base, or niche market entry. When the fit is right, strategic buyers tend to pay premium multiples because they’re not just buying cash flow; they’re buying synergies.

The businesses that attract the strongest strategic interest tend to share a few traits: loyal, diversified customer relationships; a clear and defensible niche; and operations that slot cleanly into a buyer’s existing structure. These are elements we actively engineer as part of the SMB VIG investment process, not things we hope will emerge on their own.

Sale to a Financial Buyer

Financial buyers, lower-middle-market private equity funds, independent sponsors, and family offices represent one of the most consistent and repeatable sources of liquidity in the SMB space. These buyers aren’t looking for synergies in the traditional sense. They’re looking for stable, predictable cash flows, operational improvement opportunities, and businesses that can serve as platforms for further acquisitions.

One underappreciated dynamic here is that SMBs often change hands multiple times as they scale moving from a smaller sponsor to a regional fund to a national platform. Each transition creates a liquidity event. At SMB Value Investing Group, we think about this progression deliberately when structuring deals, particularly in situations where roll-up potential exists.

Recapitalization

A recapitalization allows existing investors to realize partial or full liquidity without requiring a complete sale of the business. The most common structure involves selling a majority stake to a larger sponsor while retaining rollover equity a useful way to de-risk capital while staying exposed to future upside. Recaps can also involve debt refinancing that generates cash distributions to current owners.

These transactions are particularly well-suited to businesses that have scaled meaningfully in EBITDA, generated consistent and predictable cash flows, and are ready to transition toward institutional ownership. Many of the best-performing SMB investments we’ve seen play out exactly this way a partial exit that crystallizes value while preserving optionality.

Sponsor-to-Sponsor and Secondary Transactions

Perhaps the most structural form of liquidity in SMB investing comes from what’s sometimes called the ‘laddering effect’ the sequential movement of a platform from one financial sponsor to a larger one as it grows. An independent sponsor acquires a regional business, builds it into a multi-location platform, then sells it to a lower-middle-market fund. That fund grows it further and sells to a larger PE firm.

This is the core liquidity engine behind many SMB roll-up investment strategies. At each rung of the ladder, the business’s expanded scale, improved governance, and cleaner financials unlock a broader buyer universe and typically a higher valuation multiple. It’s a repeatable process, not a one-off event.

Exit Path Comparison at a Glance

| Exit Type | Typical Buyer | Best For | Multiple Potential |

| Strategic Sale | Corporates, Consolidators | Strong synergies, low churn | Premium (synergy-driven) |

| Financial Sponsor Sale | PE Funds, Family Offices | Stable cash flows, add-on potential | Market-rate to premium |

| Recapitalization | PE + Existing Sponsor | Scaled EBITDA, predictable cash flows | Partial liquidity and upside |

| Sponsor-to-Sponsor | Larger PE Funds | Roll-up platforms, improved governance | Scale-driven premium |

How SMB Value Investing Group Thinks About Exit Planning

At SMB Value Investing Group, exit planning is not something we do at the end of a hold period. It’s embedded in how we evaluate opportunities from day one. The SMB VIG investment process begins with a clear-eyed assessment of exit optionality: Which buyer types are realistic? What EBITDA thresholds would unlock a new pool of acquirers? What would need to be true about the business’s customer concentration, financial reporting, and operational infrastructure to make it genuinely attractive at exit?

A few principles guide our thinking consistently. We build businesses with diversified customer bases because customer concentration is one of the first things strategic and financial buyers flag in due diligence. We maintain clean, auditable financials because they compress transaction timelines and reduce buyer risk premiums. And we manage leverage conservatively not because we’re risk-averse, but because a clean balance sheet preserves optionality at every stage of the hold.

We also pay close attention to EBITDA thresholds as a strategic variable. The buyer universe for a business generating $1M in EBITDA looks meaningfully different from the one for a business at $3M or $5M. Scaling through those thresholds isn’t just a financial goal it’s a structural way to expand the list of potential exit counterparties.

Private Liquidity Is Not the Same as Public Liquidity But It’s Real

It’s worth drawing a clear distinction between the liquidity available in public markets and the kind available in private SMB investments. Public-market liquidity means you can sell a position in minutes. Private-market liquidity means you can exit a position predictably, through a well-defined process, over a period of months to years.

SMB investments are long-duration by design. That’s not a flaw; it’s the source of the return premium. But it would be inaccurate to describe quality SMBs as illiquid in any meaningful sense. Businesses with institutional characteristics diversified revenues, strong margins, professional management, and clean books are actively sought-after assets. The M&A market for them is deep and well-capitalized.

At SMB Value Investing Group, we underwrite exits conservatively. We don’t assume premium multiples. We don’t rely on a single buyer type. We stress-test our scenarios and build businesses that would be attractive across a range of market conditions. That discipline is what makes liquidity an outcome of execution rather than a matter of luck.

Key Takeaways

The lower middle market offers multiple proven exit pathways: strategic sales, financial sponsor acquisitions, recapitalizations, and sponsor-to-sponsor transactions. Each pathway rewards businesses that are well-run, simply structured, and built with institutional buyers in mind from the start. The SMB roll-up investment strategy, when executed with discipline, creates a natural progression through these exit channels as platforms grow in scale and sophistication.

If you’re evaluating SMB investments and want to understand how we apply these principles in practice, we’d welcome the conversation.