A practical comparison for high-net-worth investors weighing where to put incremental capital

For most high-net-worth investors, direct real estate has been the default alternative. It feels familiar. The underwriting is well-established. The assets are tangible. And decades of leverage-driven returns have reinforced the idea that real estate is where serious capital belongs. But at SMB Value Investing Group, we think the more honest question is this: is real estate truly the best use of incremental capital, or is it simply the most comfortable one?

This article compares SMB investing and direct real estate across the dimensions that actually matter to long-term wealth creation. Returns, risk, liquidity, leverage, and scalability. The goal is not to dismiss real estate. It is to give investors a clearer picture of what each asset class can and cannot do, so that capital allocation decisions are made deliberately rather than by default.

Why Real Estate Feels Safer Than It Is

Real estate has earned its place in private wealth portfolios. Tangible assets, predictable cash flows, established financing structures, and a long track record of inflation protection are all genuinely valuable. These are not illusions. But there is a meaningful difference between an asset class that has served investors well in a specific rate environment and one that is structurally superior across cycles.

The comfort many investors feel with real estate is partly a product of familiarity. Valuations move slowly. Downside feels visible. And early cash flow provides psychological reassurance. What this framing misses is that slow-moving valuations also mean slow-moving upside, and that comfort in familiarity is not the same thing as alpha generation.

The fundamental issue is one of return drivers. In real estate, you rarely control the underlying economic engine. Cap rate compression, rent growth, and leverage do most of the work. In SMB investing, the SMB VIG investment process is built around a different premise entirely: that outcomes can be actively shaped by the right operator, the right governance structure, and the right positioning of the business.

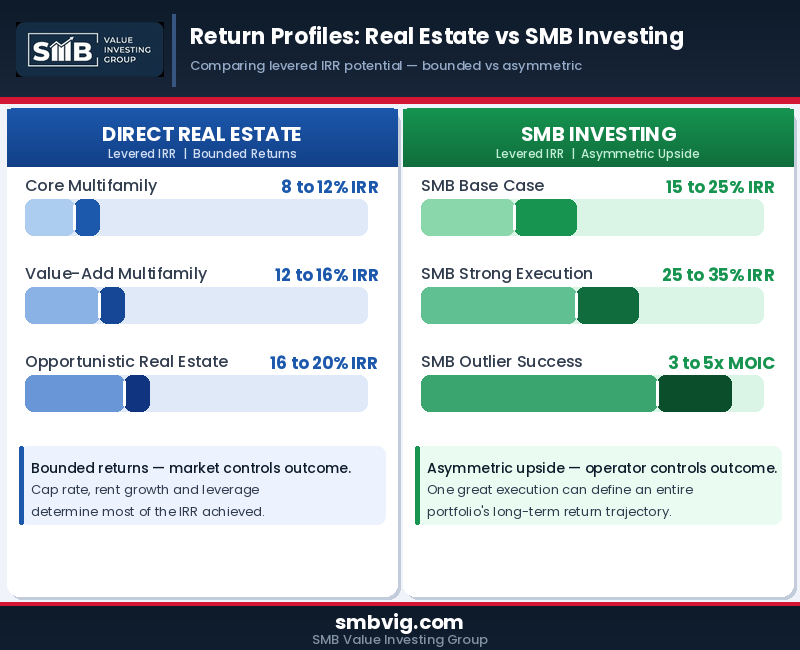

Return Potential: Bounded vs Asymmetric

The difference in return profiles between real estate and SMB investing is not just a matter of degree. It is a matter of structure. Real estate returns, even in opportunistic strategies, tend to be capped. The market determines a significant portion of the outcome. SMB investing offers something structurally different: genuine asymmetry.

Return Comparison: Real Estate vs SMB Investing

| Asset Type | Return Type | Levered IRR | Upside Ceiling |

| Core Multifamily | Real Estate | 8 to 12% | Moderate |

| Value-Add Multifamily | Real Estate | 12 to 16% | Moderate |

| Opportunistic RE | Real Estate | 16 to 20% | Capped at ~20% |

| SMB Base Case | SMB Investing | 15 to 25% | High |

| SMB Strong Execution | SMB Investing | 25 to 35% | Very High |

| SMB Outlier Success | SMB Investing | 3 to 5x MOIC | Asymmetric |

Source: SMB Value Investing Group analysis. IRR ranges are illustrative of typical market outcomes.

The numbers tell a clear story. Even in opportunistic real estate, levered IRRs tend to plateau around 20 percent. In SMB investing, a strong operator in the right business can generate 25 to 35 percent returns, and outlier outcomes, those three to five times MOIC situations, can materially redefine a portfolio. This is what small business investment returns look like when execution is strong and the business is well-selected.

Risk: The Difference Between Visible and Controllable

A common misperception is that real estate is lower risk than SMB investing. What is more accurate is that real estate risk is more visible. Interest rate movements, cap rate changes, and local supply dynamics are observable. But observable risk is not the same as manageable risk. When rates move, most real estate equity gets repriced simultaneously, and there is very little an investor can do about it.

SMB risk is different in character. Operator execution, customer concentration, and talent retention are all idiosyncratic concerns. They are specific to each business. They are also, critically, diagnosable before investment and mitigatable through active governance once capital is deployed. The SMB independent sponsor evaluation process at SMB Value Investing Group is specifically designed to assess these risks before a deal closes, not after.

This is a meaningful structural advantage. SMB risk is harder to screen for than looking at a cap rate. But once identified and underwritten properly, it can be managed in ways that market risk simply cannot.

Liquidity: Intentional vs Reactive

Real estate is often described as illiquid, but in practice many investors treat it as though it offers reliable liquidity through refinancing and partial sales. The problem is that this liquidity is entirely dependent on market conditions. When rates are rising and cap rates are expanding, refinancing becomes painful and sales timing gets forced. Liquidity that appears when conditions are favorable and disappears when you need it most is not a genuine asset.

SMB investing operates on a different model. Typical hold periods run three to seven years, and liquidity events are structured rather than reactive. Strategic sales, partial recapitalizations, and dividend distributions are planned around business performance, not external market cycles. This makes SMB liquidity more intentional and, in most cases, more value-preserving.

Leverage: Financial vs Operational

Real estate relies heavily on financial leverage. The debt enhances returns in favorable environments but creates meaningful fragility when rates move against the position. This is not a flaw unique to any particular investment. It is a structural feature of the asset class.

SMB investing uses leverage differently. Financial debt exists, but it is secondary. The primary form of leverage is operational: pricing optimization, cost structure improvement, sales efficiency, and strategic repositioning. This makes small business investment returns less sensitive to rate cycles over a full economic cycle, which is a meaningful advantage for investors with a long time horizon.

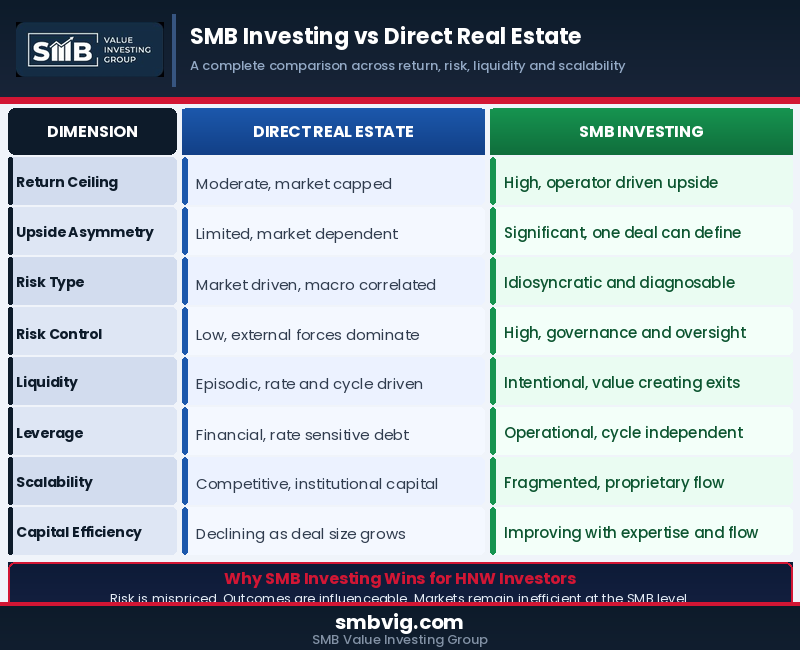

The Full Comparison: A Structured Look

SMB Investing vs Direct Real Estate: Dimension by Dimension

| Dimension | Direct Real Estate | SMB Investing |

| Return Ceiling | Moderate, bounded by market dynamics | High, operator-driven asymmetric upside |

| Upside Asymmetry | Limited, market and cycle dependent | Significant, one deal can define returns |

| Risk Type | Market-driven, macro-correlated | Idiosyncratic, diagnosable per deal |

| Risk Control | Low, external forces dominate outcomes | High, governance and active oversight |

| Liquidity | Episodic, tied to rates and market cycles | Intentional, structured value exits |

| Leverage | Financial, highly rate-sensitive | Operational, rate-cycle independent |

| Scalability | Competitive, institutional capital crowds | Fragmented, proprietary deal access |

| Capital at Work | Declining efficiency as deals grow larger | Improving with expertise and network |

Analysis by SMB Value Investing Group. For illustrative purposes.

Scalability and the SMB Opportunity

One of the most compelling aspects of the SMB opportunity for investors is what institutional capital has not yet done to the market. In multifamily real estate, large funds have compressed cap rates and commoditized underwriting across most major markets. In SMB investing, the fragmentation of the lower middle market means proprietary deal flow still exists. Businesses are frequently mispriced. Seller motivations vary widely. And experienced operators with strong networks continue to find opportunities that institutional screeners miss entirely.

The SMB opportunity size and growth thesis rests on this structural advantage. There are millions of small and medium-sized businesses in North America. A significant portion will change hands in the coming decade as baby boomer founders approach retirement. Capital is available but unevenly deployed. And operators who know how to evaluate, acquire, and grow these businesses are still generating returns that larger markets gave up years ago.

It Is Not Either/Or, But Incremental Capital Has a Better Home

The most sophisticated HNW portfolios hold both real estate and private business investments. Real estate provides inflation protection, stable cash flow, and diversification from equity market volatility. These are genuine benefits and they belong in a balanced allocation.But when the question is where incremental capital earns the highest risk-adjusted return, the answer for investors who are willing to underwrite people, operations, and execution is increasingly clear. At SMB Value Investing Group, we believe the SMB market represents one of the last remaining pockets of genuine alpha in private markets. Risk is still frequently mispriced. Outcomes are still influenceable. And for investors partnered with disciplined operators and a rigorous SMB VIG investment process, the compounding potential over a ten-year horizon is difficult to match in any traditional real estate strategy.