There are very few corners of private markets where disciplined investors still hold a structural edge. The small and medium-sized business (SMB) segment is one of them. At SMB Value Investing Group, we have spent years studying and investing in this space, and the more we look, the more conviction we carry that this asset class remains one of the most compelling and underexplored opportunities available to accredited investors today.

The question worth asking is not whether SMBs are a good investment. Decades of realized data answer that question clearly. The more important question is why this opportunity still exists and whether it will persist long enough to matter.

A Capital Gap That Institutional Investors Created

With more than $4 trillion in global private equity assets under management, it might seem like capital has found its way into every corner of the market. It has not. The vast majority of institutional capital remains concentrated in large-cap and upper-middle-market deals, where funds are deploying $500 million to $10 billion per vehicle. In that world, a $5 to $20 million equity check is simply too small to justify the sourcing, diligence, and management overhead required.

As a result, the SMB segment (specifically businesses generating $2 to $10 million in EBITDA) has been systematically undercapitalized. These are not weak businesses. They are operationally sound, cash-generative companies that happen to be too small for large funds and, in many cases, too complex or expensive for individual buyers to acquire outright. That gap is not a market flaw. For investors who understand how to navigate it, it is a durable structural advantage.

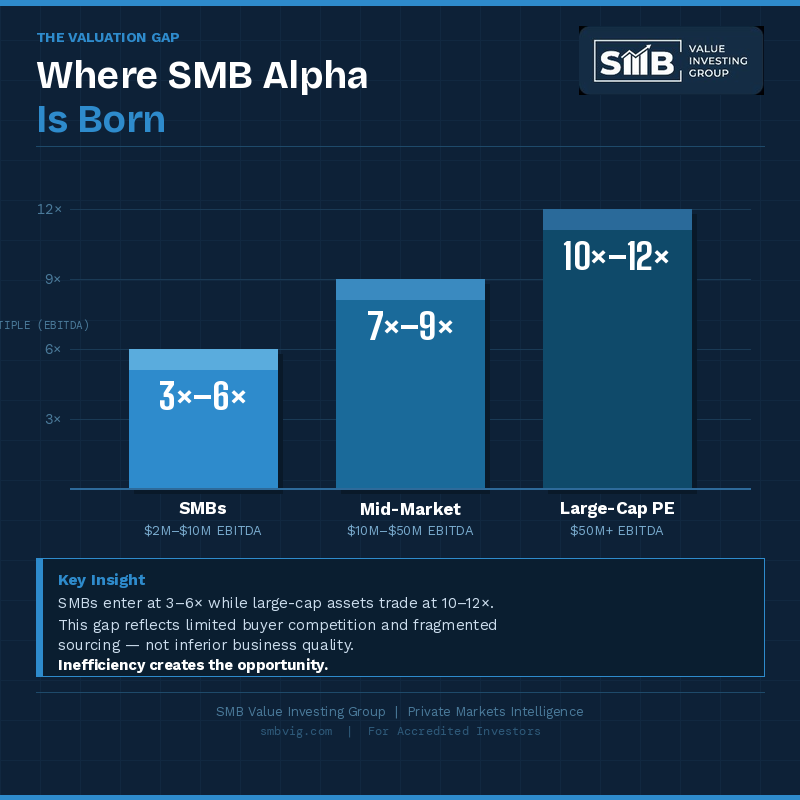

The Valuation Gap Is Real and Persistent

One of the most compelling aspects of the SMB market is the pricing differential compared to larger private equity targets. The table below illustrates how dramatically entry multiples vary across market segments:

| Segment | Typical EBITDA Range | Average Entry Multiple |

| SMBs (Lower Middle Market) | $2M – $10M | 3× – 6× EBITDA |

| Mid-Market PE Targets | $10M – $50M | 7× – 9× EBITDA |

| Large-Cap / Upper Middle Market | $50M+ | 10× – 12× EBITDA |

This valuation gap is not a reflection of inferior business quality. It reflects reduced buyer competition, minimal broker involvement, and the complexity premium that most capital sources demand. Inefficiency, not inferiority, is what keeps SMB multiples low. For investors with the right investment criteria for small businesses, this is precisely where value is created.

Why the Fragmentation Works in Our Favor

SMBs typically operate in fragmented industries such as B2B services, specialty manufacturing, niche distribution, and similar verticals. These markets lack centralized data, standardized reporting, and consistent broker coverage. For large institutions optimized around auctions and scale, this fragmentation is a barrier. For a firm like SMB Value Investing Group, it is an advantage.

Because deals are sourced through relationships rather than competitive processes, entry prices tend to be lower and deal structures tend to be more favorable. The absence of institutional intermediaries also means there is more room to negotiate terms that provide genuine downside protection in SMB acquisitions, including earnouts, seller notes, structured equity, and other mechanisms that are increasingly rare in larger, more intermediated transactions.

What the Data Actually Shows

This is not a theoretical opportunity. The Stanford Graduate School of Business Search Fund Study, updated in 2024, documented approximately 35 percent gross IRR and roughly 4.5 times multiple of invested capital across more than four decades of realized outcomes in this segment. The McGuireWoods Independent Sponsor Survey from the same year found that independent sponsor transactions outperform traditional PE on a risk-adjusted basis, in large part because deal-by-deal capital structures enforce discipline that institutional funds sometimes lack.

| Source | Gross IRR | Multiple of Capital (MOIC) |

| Stanford Search Fund Study (2024) | ~35% | ~4.5× |

| McGuireWoods Independent Sponsor Survey (2024) | Outperforms traditional PE (risk-adjusted) | N/A (deal-by-deal) |

These results were not driven by financial engineering. They were driven by lower entry multiples, operational improvements, and selective add-on acquisitions that expanded scale over time. That is exactly the playbook SMB Value Investing Group focuses on.

The Operator Question Is the Real Differentiator

Capital alone does not eliminate inefficiency in the SMB market. Execution does. Many small businesses arrive with informal financial reporting, minimal KPI tracking, and operations that are built around a founding owner rather than scalable systems. These characteristics deter institutions, but for capable operators, they represent clear and measurable value-creation opportunities.

At SMB Value Investing Group, we place significant emphasis on high-performing SMB operators as the core of our investment thesis. Finding and backing the right operator, someone who can step into a business, stabilize it, and execute a defined improvement plan, is where we believe the most durable alpha is generated. It is not enough to buy at a low multiple. The business has to be in the right hands.

Why This Window Will Not Close Overnight

Some investors worry that the SMB opportunity is crowded. We understand the concern, but the data does not support it. Family offices and accredited investors are gradually entering the space, independent sponsor platforms continue to grow, and the ecosystem is slowly professionalizing. However, institutional capital simply cannot absorb millions of small deals. Fragmentation and execution complexity are structural features of the market, not temporary frictions.

The accredited investor investment process in this space is also more selective and relationship-driven than most institutional channels. That selectivity, while sometimes frustrating for deal flow, acts as a natural filter that keeps the market from being quickly arbitraged away. We expect the SMB opportunity to remain viable across multiple market cycles, though the investors who enter with discipline and strong operator relationships will continue to outperform those who enter on capital alone.

How SMB Value Investing Group Approaches This Market

Our approach at SMB Value Investing Group is built on four principles that reflect the realities of this asset class. We target lower entry multiples through proprietary sourcing rather than auction processes. We build downside protection into every deal structure so that investors have meaningful safeguards if a business underperforms expectations. We apply rigorous investment criteria for small businesses predictable cash flows, clear competitive positioning, and defensible margins. And we prioritize operator quality above all else.

This is not a strategy for investors seeking quick liquidity or passive exposure. It is for accredited investors who are willing to accept a degree of complexity in exchange for access to returns that are genuinely differentiated from public markets and large-cap private equity.

Final Thoughts

The SMB market is where inefficiencies still exist in private equity – and where disciplined investors can capture real alpha before capital inevitably scales down-market. The opportunity is real, it is backed by decades of performance data, and it is still early enough to matter.

At SMB Value Investing Group, we believe the investors who approach this space with patience, rigor, and the right operator relationships will continue to find compelling opportunities for years to come. If you are an accredited investor exploring this space, we welcome the conversation.