At SMB Value Investing Group (SMB VIG), we spend a great deal of time evaluating individual businesses. But if we are being honest about what actually drives long-term performance in private markets, the answer is not just which businesses you choose. It is how you put them together.

Small and medium-sized business investing is one of the most compelling small business investment opportunities available in private markets today. The return potential is real. So is the risk. And in a world where portfolios are concentrated, positions are illiquid, and outcomes depend almost entirely on execution, the way you construct a portfolio is not a secondary concern. It is the primary risk management tool you have.

This article walks through the framework behind the SMB VIG investment process, explaining how we think about building portfolios that can absorb mistakes, benefit from winners, and compound over time.

Why SMB Portfolios Require a Different Mental Model

Most investment frameworks were designed for public markets, where you can hold hundreds of positions, exit within seconds, and count on statistical diversification to smooth out rough patches. None of those conditions apply to SMB investing.

A typical SMB portfolio holds between fifteen and twenty-five investments. Each one is illiquid for three to seven years. Each outcome is shaped more by the operator, the business model, and timing than by broad market movements. There is no law of large numbers working in your favor. One poorly sized mistake can do real damage.

This is the starting point for everything we do at SMB Value Investing Group. We treat each allocation as if it might be the only investment we make. That discipline forces the right questions before capital ever moves.

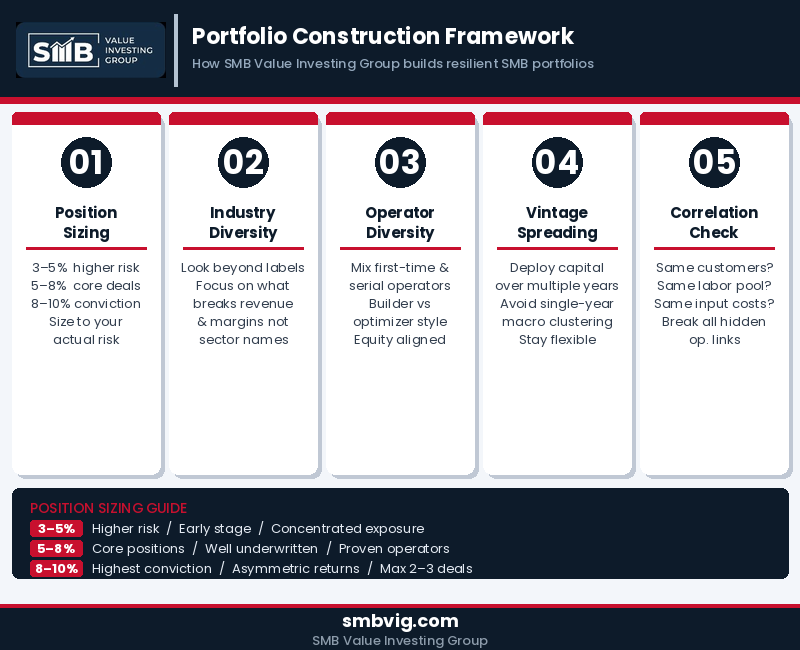

Position Sizing: The Decision That Defines Everything Else

Position sizing is the most consequential decision in a concentrated portfolio. Get it right and you can survive bad outcomes and let good ones run. Get it wrong and a single deal can set back years of progress.

Our general framework at SMB VIG runs along three tiers. Early-stage or higher-risk positions typically represent three to five percent of the portfolio. Core, well-underwritten investments sit in the five to eight percent range. The very rare, highest-conviction opportunities with genuine asymmetric return potential can reach eight to ten percent, though we approach that ceiling with care.

The underlying principle is simple: no single investment should be capable of permanently impairing your portfolio.

Sizing Reflects Risk, Not Just Return Potential

Two deals can look equally attractive on paper while carrying very different risks. Part of what defines good SMB investment criteria is the discipline to adjust position size based on real-world risk variables rather than projected returns alone.

Customer concentration is one of the most common risks in small business deals. A business that depends on one or two clients for the majority of its revenue carries a fragility that is rarely reflected in its valuation. Similarly, businesses with heavy capital expenditure requirements, significant regulatory exposure, or deeply cyclical revenue profiles all warrant tighter initial sizing. On the other side, recurring revenue, experienced management, and mission-critical relationships with customers support larger allocations. The goal is to be appropriately compensated for the risks you take.

Industry Diversification: It Is About Economics, Not Labels

When most investors think about industry diversification, they think in terms of sectors. Healthcare. Technology. Manufacturing. In SMB investing, that kind of surface-level thinking is not enough.

Two businesses in different sectors can share the same economic vulnerability. A regional staffing firm and a light manufacturer might look diversified by label, but if both are sensitive to the same local labor market dynamics, they are likely to face stress at the same time. True diversification means understanding what actually causes revenue and margins to break, and ensuring that your portfolio does not have too many businesses where the answer is the same thing.

Within the SMB VIG investment process, we think of industry exposure in terms of economic drivers rather than sector labels. Mission-critical B2B services tend to behave defensively. Healthcare services are resilient but carry regulatory complexity. Light manufacturing and construction-adjacent businesses are meaningfully cyclical. The question before any new investment is not just what industry the business is in. It is what would have to go wrong for this business to underperform, and whether that scenario is already well-represented in the portfolio.

Operator Diversification: People Risk Is Portfolio Risk

In large-cap private equity, institutional processes provide some buffer against individual performance. In SMB investing, there is no such buffer. The operator is often the business. Their judgment, their energy, and their ability to execute under pressure are the primary determinants of whether an investment succeeds or struggles.

This makes operator diversification a structural part of how we build portfolios at SMB Value Investing Group. Two deals in completely different industries can be highly correlated if both are run by first-time operators following the same playbook. A portfolio concentrated in finance-led acquirers who prioritize deal engineering over operational improvement carries a hidden consistency of risk.

We look at operator background, experience level, management style, and incentive structure when assessing whether a new investment genuinely adds diversity to the portfolio or simply adds more of the same. Meaningful equity alignment matters. An operator with real skin in the game responds differently under pressure than one drawing primarily a salary.

Vintage Diversification: When You Enter Shapes What You Earn

Improving small business investment returns over time is not just about picking better businesses. It also requires thinking carefully about when you deploy capital.

SMB investments are long-duration assets. The valuation environment at entry, the leverage assumptions embedded in the deal, and the macro backdrop against which the business will need to execute all matter. Deploying most of a portfolio’s capital in a single year at similar multiples and similar leverage levels concentrates timing risk in ways that compound other risks.

A deliberate deployment curve spread across several years reduces this exposure. Early investments inform later ones. Selection improves as the team builds pattern recognition. And the portfolio avoids being uniformly exposed to a single macro environment, whether that turns out to be benign or difficult.

Operational Correlation: The Risk That Hides in Plain Sight

A portfolio can look well-diversified on a sector allocation chart while carrying deep operational correlations that only surface under stress. This is one of the more underappreciated risks in SMB investing, and it is worth examining carefully before committing to any new position.

The questions we ask at SMB Value Investing Group are practical. Do multiple portfolio companies sell into the same customer vertical? Do they compete for the same labor pool? Are they geographically concentrated in a way that creates shared exposure to a regional slowdown? Do their margins depend on the same input costs, whether that is freight, energy, materials, or professional services rates?

If the answers cluster, the portfolio is more correlated than it appears. Addressing this means actively breaking those operational links, not just ensuring that businesses carry different industry labels.

Rebalancing Without the Ability to Sell

In public markets, rebalancing is mechanical. You trim what has grown too large and add to what has shrunk. In illiquid SMB investing, that option does not exist in the same form. Rebalancing is instead a forward-looking discipline. It means allocating future capital with full awareness of where the existing portfolio is already exposed.

At SMB Value Investing Group, we treat rebalancing as an ongoing practice rather than a periodic event. When a company significantly outperforms expectations, its relative weight in the portfolio grows. Future allocations should compensate by introducing exposure to different industries, operators, or entry environments. When confidence in an operator’s execution erodes, similar operator profiles are deprioritized in new commitments. And when structural changes affect a sector already represented in the portfolio, existing exposure is evaluated more conservatively.

One of the most underused rebalancing tools is dry powder. Maintaining intentional reserves gives investors the flexibility to act on exceptional opportunities later in the deployment cycle without being forced to redeploy prematurely.

The Pre-Investment Checklist

Before committing new capital, the SMB VIG investment process includes a final portfolio-level review. This is not a scoring exercise. It is a discipline.

The questions are straightforward. Will this push any industry or economic driver above its target weight in the portfolio? Does it concentrate exposure to a risk already well-represented? Is this operator type already familiar, or does it genuinely add something different? Does the timing cluster too closely with recent deployments? And most importantly, is the return potential sufficient to justify the incremental risk being added?

If multiple answers raise concern, the right response is not to rationalize the investment. It is to resize, restructure, or pass.

Final Thought: The Portfolio Is the Product

There is a natural temptation in private market investing to focus on individual deal quality. Find great businesses. Avoid bad ones. The problem is that even a portfolio of individually good businesses can produce disappointing outcomes if it is assembled carelessly.Great SMB investing is not about picking only winners or avoiding all losses. It is about sizing mistakes so they do not define results, letting real winners matter, and surviving long enough to let compounding do its work. That is the philosophy behind every small business investment opportunity we evaluate at SMB Value Investing Group, and it is what drives the long-term discipline of the SMB VIG investment process.