MOIC vs IRR: Which Metric Matters More for SMB Investors?

And when each metric can quietly mislead you

In private markets, few numbers get quoted more often or understood less carefully than IRR and MOIC. Every independent sponsor deck, every CIM, every investment memo will show you both. But here is the thing: most investors have a habitual preference for one without ever examining what the other is actually telling them. At SMB Value Investing Group, we spend a significant amount of time helping investors understand why both metrics matter, why neither is sufficient on its own, and how the small business investment process changes the conversation entirely.

This guide is written for serious investors who want a cleaner mental model — not a formula, but a way of thinking that holds up under pressure when real capital is at stake.

The Definitions Worth Getting Right

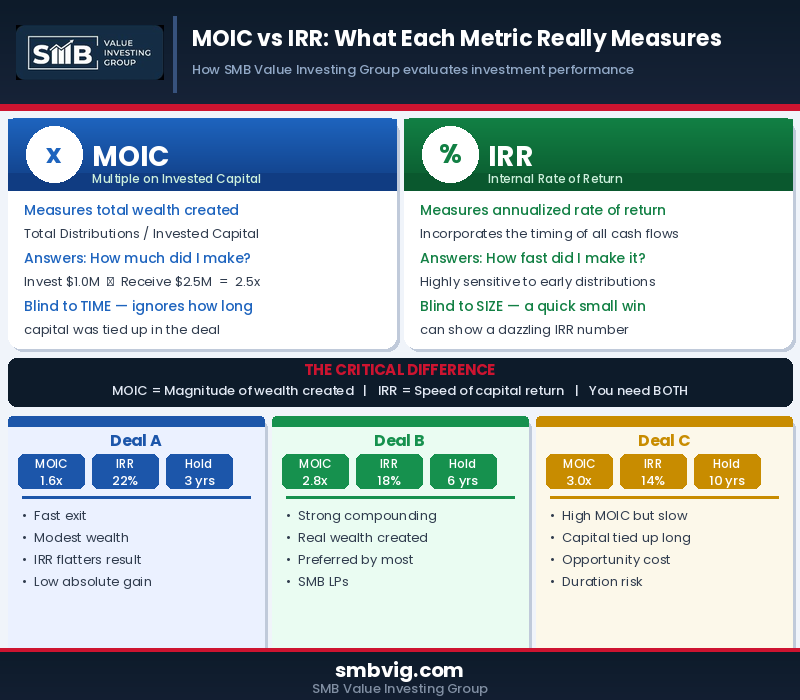

MOIC — Multiple on Invested Capital answers a simple question: how many dollars did you get back for every dollar you put in? If you invest one million and receive two and a half million in total distributions, your MOIC is 2.5x. It is a measure of magnitude. It tells you how much wealth was created, full stop.

IRR Internal Rate of Return answers a different question: how fast did your money grow? It is an annualized rate that incorporates the timing of every cash flow. A 2.5x MOIC achieved in three years produces a dramatically different IRR than the same multiple achieved over eight. IRR rewards speed. MOIC rewards scale.

Neither question is wrong. But each tells only part of the story, and in SMB investing, leaning on just one of them is how investors end up drawing the wrong conclusions.

Why IRR Can Mislead You in SMB Deals

IRR is a powerful tool, but it has structural weaknesses that are especially relevant in the SMB context.

Early Cash Flows Distort the Picture

IRR is highly sensitive to when cash flows arrive. If a deal returns a meaningful distribution in Year 1 through a refinancing or recap, the IRR calculation is turbocharged even if the remaining hold generates modest additional value. An investor can look at a 22 percent IRR and feel very good about a deal that ultimately only returned 1.6x invested capital. That is not a great outcome. The speed flattered the result.

Short Holds Inflate the Number

A quick exit almost always produces an impressive IRR, even when absolute profits are limited. This matters in SMB investing because early recapitalizations and partial exits can front-load returns while leaving the longer-term fundamentals weakened. The IRR looks strong. The actual wealth creation does not match.

The Reinvestment Assumption Is Often Unrealistic

IRR implicitly assumes that all interim cash flows are reinvested at the same IRR. In reality, capital sits idle between deals, future SMB investment opportunities for investors may carry different risk profiles, and reinvestment is never guaranteed. This assumption quietly undermines IRR as a standalone performance metric for most individual LPs.

Why MOIC Can Mislead You Too

MOIC has its own blind spots, and they are just as dangerous.

The core issue is that MOIC is completely indifferent to time. A 2.5x return in five years is a genuinely strong result. A 2.5x return in twelve years is a very different story — the opportunity cost of capital tied up for that long significantly changes the risk-adjusted value of the outcome. High MOIC numbers can also hide capital inefficiency. A deal that produces 3.0x but takes a decade with no interim cash flow may look attractive on paper while being inferior to a more modest multiple achieved with better capital velocity. This is where the SMB investment criteria used by sophisticated LPs go well beyond headline multiples.

Three Deals, Three Very Different Stories

The table below illustrates how the same headline numbers can mean very different things depending on context.

Deal Comparison: MOIC vs IRR vs Hold Period

| Deal | MOIC | IRR | Hold Period | Interpretation |

| Deal A | 1.6x | 22% | 3 years | Fast exit with modest wealth creation. IRR flatters the result. |

| Deal B | 2.8x | 18% | 6 years | Strong compounding. Real wealth created. Most LPs prefer this outcome. |

| Deal C | 3.0x | 14% | 10 years | High MOIC but significant duration risk. Capital efficiency is weak. |

Source: SMB Value Investing Group illustrative analysis. Not a representation of actual fund performance.

Most experienced SMB investment professionals would choose Deal B not because it has the highest IRR or the highest MOIC, but because it reflects strong compounding with genuine wealth creation and reasonable capital efficiency. Deal A flatters with speed. Deal C impresses with magnitude but penalizes with time.

MOIC vs IRR: What Each Metric Really Measures

Why SMB Investing Changes This Debate

SMB deals have structural characteristics that shift the MOIC versus IRR conversation. Unlike venture capital, where holds can stretch to twelve years or longer and cash flow is rare until exit, small businesses typically generate income from day one. Distributions happen during the hold. Exit timelines run four to seven years, not ten to twelve.

These characteristics reduce the distortions that make IRR unreliable in long-duration assets, while making MOIC a more genuine reflection of real returns. In a cash-flowing SMB deal, MOIC captures real wealth creation. IRR captures capital discipline and efficiency. The small business investment process at SMB Value Investing Group evaluates both together, alongside hold period and interim cash flow, to form a complete picture.

The Complete Framework: MOIC x IRR x Time

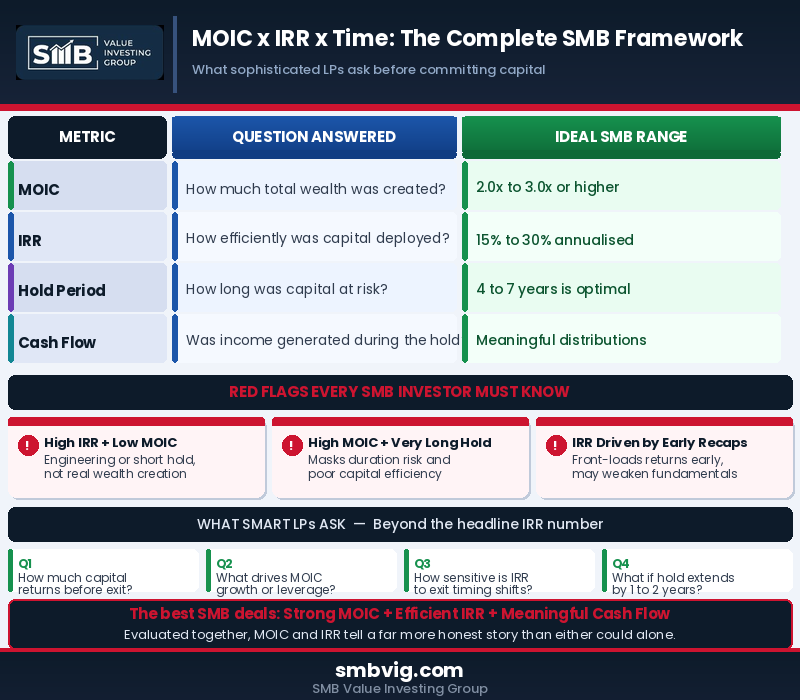

Sophisticated LPs do not evaluate deals on a single metric. They triangulate across three dimensions simultaneously.

| Metric | Question Answered | Ideal SMB Range |

| MOIC | How much total wealth was created? | 2.0x to 3.0x or higher |

| IRR | How efficiently was capital deployed? | 15% to 30% annualised |

| Hold Period | How long was capital at risk? | 4 to 7 years optimal |

| Cash Flow | Was income generated during hold? | Meaningful distributions |

Framework applied within the SMB VIG investment process.

MOIC x IRR x Time: The Complete SMB Framework

Red Flags That Every LP Should Recognize

High IRR with Low MOIC

This combination almost always suggests financial engineering, early recaps, or a very short hold. The speed impresses, but the absolute wealth creation is insufficient. Do not let a headline IRR number end the conversation before it starts.

High MOIC with a Very Long Hold

Three times your money sounds excellent. Three times your money over ten years with no interim cash flow is a much harder case to make. Duration risk is real, and it compounds quietly. This is one of the most overlooked areas in evaluating what appears to be a strong outcome.

IRR Driven Primarily by Early Recaps

This is the most subtle red flag. When a deal’s IRR is dominated by a Year 1 or Year 2 recap rather than by sustained business performance the IRR can look strong while the underlying fundamentals may actually be weaker than they appear. Always ask what is driving the metric.

What Smart LPs Ask Before Committing Capital

Rather than asking only what the IRR is, investors who understand the SMB investment opportunities for investors landscape ask a deeper set of questions. How much capital is expected to return before the exit event? What specifically drives the MOIC projection is it revenue growth, margin expansion, or financial leverage? How sensitive is the IRR to exit timing, and what happens if the hold extends by one or two years? These questions reveal the economic quality of a deal that the headline numbers alone simply cannot.

The Bottom Line

IRR and MOIC are tools, not verdicts. IRR without MOIC context can exaggerate success. MOIC without time context can hide inefficiency. For investors navigating SMB investment decisions, the goal is never to maximize a single metric. It is to compound capital intelligently while managing duration risk and generating meaningful cash flow along the way.At SMB Value Investing Group, we believe the best deals create real absolute wealth, use time efficiently, and put cash in investor pockets during the hold — not just at exit. When MOIC and IRR are evaluated together, with honest attention to the hold period, they tell a far more complete and reliable story than either ever could alone.